At Glenys and Mark Sequeira

We're your Trusted Partners in charting the course to lasting wealth and success.

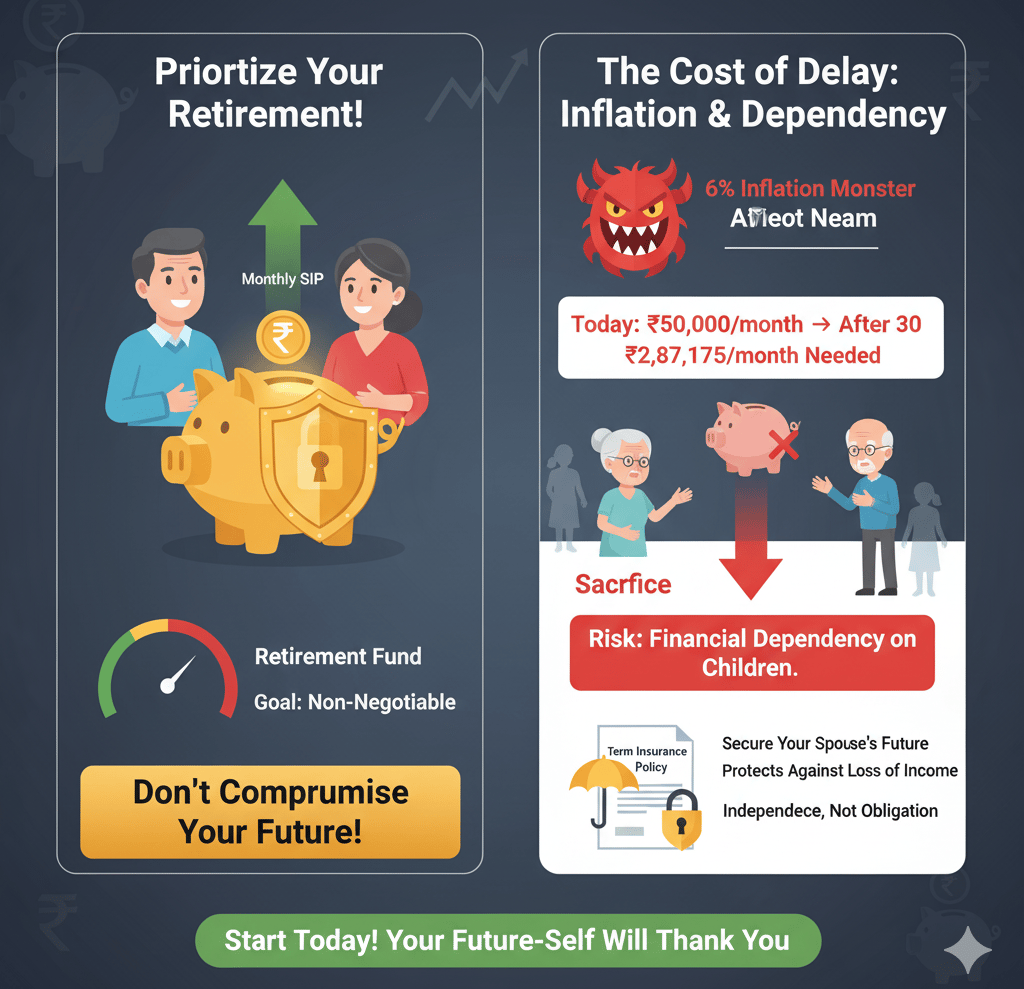

🛑 Stop Sacrificing Your Future: Why Your Retirement is Your Most Important Financial Goal

In the Indian family context, a deeply ingrained cultural expectation often compels parents to prioritize their children's education, marriage, and financial security, sometimes at the expense of their own well-being. This noble sacrifice, however, is leading to a silent crisis: a generation of financially dependent retirees

11/9/20252 min read

In the Indian family context, a deeply ingrained cultural expectation often compels parents to prioritize their children's education, marriage, and financial security, sometimes at the expense of their own well-being.1 This noble sacrifice, however, is leading to a silent crisis: a generation of financially dependent retirees.

It is time for a paradigm shift. Your Retirement Goal should be a non-negotiable, sacred commitment, protected above all else. Saving for your retirement is not selfish; it is the most responsible act you can take for your future self and, ironically, for your children.

📉 The Inflation Monster: Your Rs 50,000 Today Will be a Pittance Tomorrow

The biggest destroyer of a sound financial plan is often underestimated: inflation. Many people calculate their retirement needs based on today’s expenses, completely ignoring how rapidly the cost of living will soar.

Let's look at a simple, stark calculation:

Current Monthly Expense: ₹50,000

Time to Retirement: 30 Years

Assumed Annual Inflation Rate: 6%

Future Monthly Expense (after 30 years)₹2,87,175 (Approx.)

The Reality Check: To maintain your current standard of living of ₹50,000 per month, you will need nearly ₹2.87 Lakh per month just 30 years from now. If you compromise your retirement savings for other goals, you will fall catastrophically short of this figure. Your financial plan will be destroyed, and you will be forced to depend on the very children you tried so hard to protect.

🎯 Non-Negotiable Financial Mandates for a Secure Retirement1. Secure Your Retirement Fund First

Your retirement savings should be treated as a fixed monthly expense, like rent or an EMI, not a discretionary surplus.

Automation: Set up an automatic Systematic Investment Plan (SIP) into a diversified portfolio (equity mutual funds for long-term growth) on the very first day you receive your salary. This eliminates the temptation to divert funds.

Reverse Planning: Calculate the total corpus you need at retirement (using the inflation-adjusted expense shown above) and then work backward to determine the monthly SIP required. This provides a clear, motivating target.

2. Your Spouse’s Security is Paramount: The Term Policy Shield

The single largest threat to your spouse's retirement security, especially if they are a non-earning or lower-earning partner, is the loss of your income.

Do not rely on children: Children have their own lives, careers, and financial burdens (including the future cost of their own children's education!). Expecting them to fund your spouse's life is a risky and outdated model.

The Power of Term Insurance: Secure your spouse's future with an adequate Term Insurance Policy (or a Joint Life Term Plan). This policy is the ultimate safety net. In the unfortunate event of your demise, the lump sum payout is designed to replace your future income, ensuring your spouse can live a financially independent life and achieve the retirement you both planned for. This payout provides an instant, large corpus that can be invested to fund their needs, without any dependence on the next generation.

Crucial Tip: A term plan is pure protection, offering a large cover at a minimal premium. It is the cheapest and most effective way to secure a family's financial future against the risk of the breadwinner's premature death.

🔑 Final Word: Responsibility, Not Dependency

The true legacy you can leave your children is the gift of freedom from obligation. When you achieve financial independence in your retirement, your children are free to pursue their own goals without the heavy financial burden of caring for you.

Start today: Pay yourself first, protect your spouse second, and let your children pursue their dreams without financial guilt or compulsion.