At Glenys and Mark Sequeira

We're your Trusted Partners in charting the course to lasting wealth and success.

💀 The Fixed Deposit Trap: How Safety Can Destroy Multi-Generational Wealth

11/9/20252 min read

💀 The Fixed Deposit Trap: How Safety Can Destroy Multi-Generational Wealth

For decades, the Fixed Deposit (FD) has been championed as the epitome of financial safety in India. While this security is appealing, particularly to risk-averse investors and those planning for short-term needs, relying on FDs for long-term wealth creation, especially for passing on a substantial legacy, can be a monumental mistake. The seemingly safe choice can, paradoxically, become an engine of wealth destruction, largely due to two silent killers: low returns and inflation.

This is the story of Ramesh and Suresh, two brothers who inherited the same financial start but chose fundamentally different paths, leading to vastly divergent outcomes over a 50-year horizon.

📈 The Tale of Two Brothers: Ramesh vs. Suresh

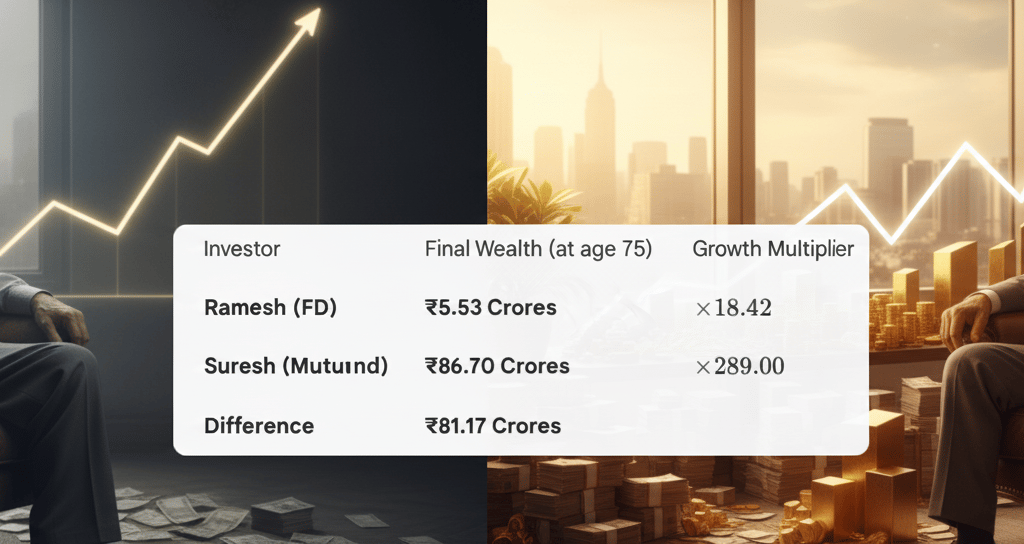

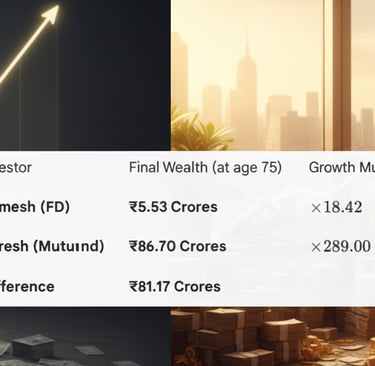

Ramesh and Suresh, at age 25, each inherited ₹30 Lakhs from their mother. They had fifty years until retirement to grow this legacy.

Ramesh: The FD Investor

Ramesh chose the comfort of a Fixed Deposit, accepting a guaranteed but modest 6% annual return. He valued certainty above all else. After 50 years, Ramesh's total wealth is approximately ₹5.53 Crores.

Suresh: The Balanced Mutual Fund Investor

Suresh accepted a higher but manageable risk, investing in a Balanced Mutual Fund (a mix of equity and debt) which, historically, can deliver higher returns over the long term. He assumed an annual return of 12%.

After 50 years, Suresh's total wealth is approximately ₹86.70 Crores.

🤯 The Legacy Destroyed vs. The Legacy Secured

The difference in wealth is staggering, and it's all due to the power of compounding applied to a relatively small difference in the rate of return (6% vs. 12%).

The FD destroyed the potential multi-generational wealth. Ramesh's ₹5.53 Crore portfolio, while numerically larger, is barely enough to fund a single retirement and a small legacy, especially when accounting for inflation.

Suresh's ₹86.70$ Crores portfolio represents true multi-generational wealth. It is a financial fortress capable of supporting his retirement and providing substantial, life-changing inheritances for his children and grandchildren.

🔥 The Silent Killer: Inflation

The stark contrast is amplified when factoring in inflation, the true destroyer of fixed-income returns.

If the average inflation rate over those 50 years was 5%, we must look at the real rate of return.

Ramesh's Real Return: 6 %(FD Return)} - 5% (Inflation)} = 1% Real Return

Suresh's Real Return: 12 %(MF Return)} - 5% (Inflation)} = 7% Real Return

Ramesh's wealth grew by only 1% in real terms. While he made a profit on paper, the purchasing power of his money barely increased. The ₹5.53 Crores he earned will buy only a little more than the initial ₹30 Lakhs could 50 years prior, thus destroying the legacy's real value.

Suresh's 7% real return is the engine that created the ₹86.70 Crores of real, impactful wealth, ensuring his mother's legacy not only survived but flourished for future generations.

💡 The Takeaway for Multi-Generational Wealth

For wealth intended to last decades and cross generations, the primary financial goal must be to beat inflation by a significant margin. This requires allocating a substantial portion of the portfolio to growth assets like equities, via instruments like mutual funds, which have the potential to deliver high double-digit nominal returns over the long run.

Fixed Deposits are suitable for:

Emergency Funds: Money needed in 6-12 months.

Short-Term Goals: Funds for a down payment or vacation in 1-3 years.

Capital Preservation: For those already wealthy who cannot afford to lose any capital.

However, for those starting out or looking to create a true, enduring family fortune, embracing the managed risk of growth assets is not a choice—it is a necessity. The failure to do so, as demonstrated by Ramesh, is a guarantee that the promise of multi-generational wealth will be severely curtailed, if not entirely destroyed.