At Glenys and Mark Sequeira

We're your Trusted Partners in charting the course to lasting wealth and success.

⏳ The Power of Starting Early: Securing Your Child's Education Fund with an SIP

Blog post description.

11/9/20252 min read

⏳ The Power of Starting Early: Securing Your Child's Education Fund with an SIP

One of the most valuable gifts a parent can give a child is a secure financial foundation for their education. Planning early is crucial, and a Systematic Investment Plan (SIP) in mutual funds, harnessed by the power of compounding, is an excellent way to achieve this goal.1

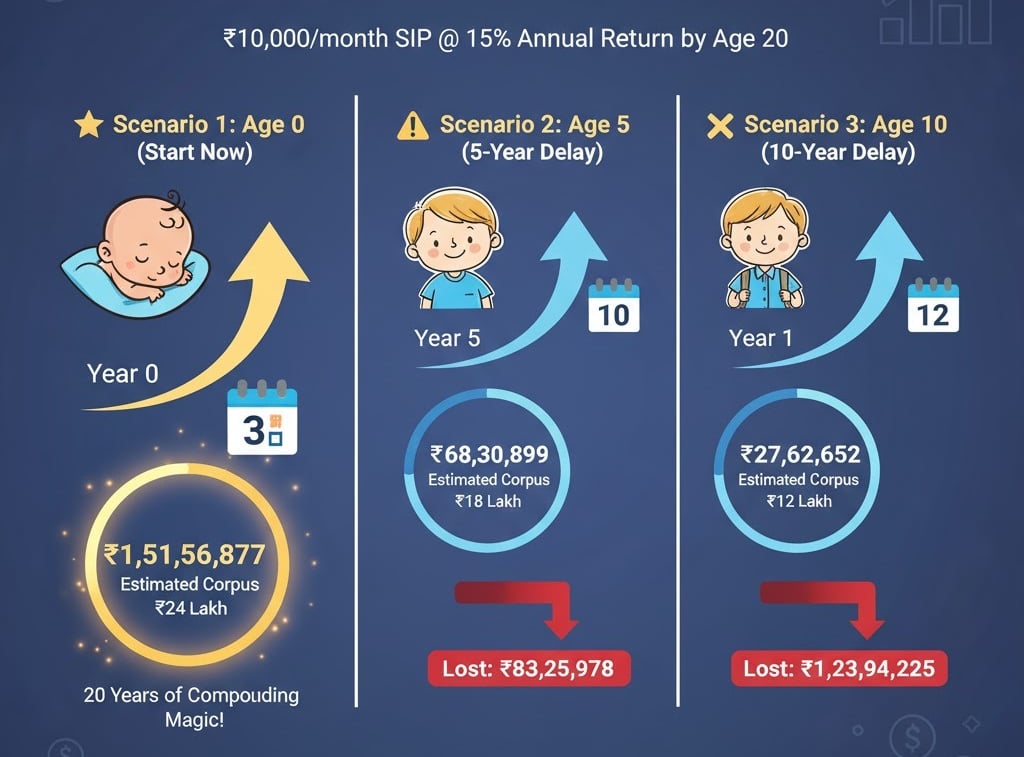

This article illustrates how a simple SIP of ₹10,000 per month, started from the child's birth (age 0), can build a substantial education corpus by the time they turn 20, assuming a modest annual return of 15%. Crucially, we'll also demonstrate the significant financial cost of delaying this start.

🌟 Scenario 1: The Disciplined Early Start (Age 0)

Starting a monthly SIP of ₹10,000 immediately at the child's birth gives your investment the maximum time—20 years—to grow. Over two decades, compounding works its magic, ensuring that not only your principal but also the returns from previous periods start earning returns themselves.2

Monthly SIP of Rs 10,000 over 20 years from Age o to Age 20. Total invested Rs 24Lacs at 15% that is Rs 1.51Cr

By starting early, your invested amount of ₹24 Lakhs grows over six times to an estimated corpus of over ₹1.5 Crore! This sizable amount can provide a comfortable cushion for most higher education expenses, be it in India or abroad.

⚠️ The Cost of Delay: How Procrastination Erodes Your Corpus

Life often gets in the way, and many parents delay their child's education planning. The following scenarios demonstrate the massive financial loss incurred by delaying the same ₹10,000 monthly SIP by just 5 or 10 years.

Scenario 2: Delay of 5 Years (Starting at Age 5)

If you delay the SIP for five years, you lose the crucial early period of compounding.

Monthly SIP₹10,000 Duration15 Years (Age 5 to Age 20) Total Investment (Principal) Rs10,000 per year for 15 years. Total invested Rs 18lacs Expected Annual Return15% Estimated Corpus Value ₹68,30,899 (Approx. ₹68.31 Lakh)

Amount Lost due to Delay (vs. Age 0) - ₹83,25,978

Scenario 3: Delay of 10 Years (Starting at Age 10)

A further delay of five years (a total of 10 years) drastically reduces the accumulation time, magnifying the loss.

SIP₹10,000 Duration10 Years (Age 10 to Age 20) Total Investment (Principal) Rs 12,00,000

Expected Annual Return - 15% Estimated Corpus Value - ₹27,62,652 (Approx. ₹27.63 Lakh)

Amount Lost due to Delay (vs. Age 0)₹1,23,94,225

Key Insight: Starting at Age 5 means losing nearly ₹83 Lakh compared to starting at Age 0. Starting at Age 10 means losing over ₹1.23 Crore. The difference is primarily due to the power of compounding having fewer years to accelerate the growth of the corpus.

🎯 Conclusion: Start Early, Start Now

The difference between a multi-crore education fund and a modest one often comes down to just one factor: Time.

Starting an SIP early ensures your money works hardest during the crucial initial years, making up a significant portion of the final wealth. While market returns (like the 15% assumed here) are never guaranteed and carry risks, the mathematical impact of time remains constant.

Don't wait for a better market moment, a higher salary, or the perfect fund. The single most powerful step you can take for your child's future is to start that SIP today.